Building the best strategy starts with pinpointing your benefit at different ages.

Back in the late 1980s, when much like today there was mounting concern about the future of Social Security, Congress decided to reassure anxious Americans by sending them a notice every year highlighting what their future benefits would be. Workers whose pay stubs showed exactly how much tax they are paying into the system every payday would at least get a once-a-year reminder of the reward at the end of the road. By 1999, the government was printing and mailing more than 150 million Social Security statements annually. In 2011, though, the agency abandoned the program in order to save about $60 million a year in printing and postage costs. (You call that reassuring?) The agency has since come up with the cash to mail paper statements to workers every five years starting when they turn 25, and then every year once they reach age 60 until benefits start.

But you don’t have to wait for the mail. A regularly updated, personalized statement showing your lifetime earnings record and estimates of future benefits is always as close as your computer. To see what Social Security has for you, visit www.ssa.gov/mystatement. Setting up an account will take a few minutes and require that you answer some questions that might make you wonder how the Social Security Administration knows the answers—such as the name of the bank where you applied for a home equity loan, the name of your high school or the number of bedrooms in your home. Your answers are compared with information maintained by a credit reporting bureau as a means to verify your identity. (Don’t be thrown for a loop if you’re asked about something that doesn’t exist, such as a home equity loan. Just choose the “none of the above” response.)

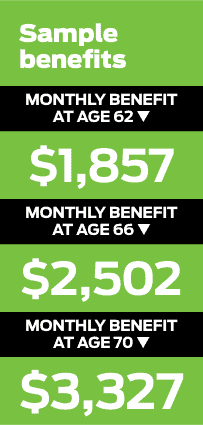

Once you have your username and password, you’ll have access to your Social Security statement. It contains a treasure trove of information. Of immediate interest is sure to be the estimate of how much you can expect to receive each month once you retire. Each year, the government announces the “average” Social Security benefit for all retired workers. For 2016, it’s $1,340. What your statement delivers is a personalized estimate of what you will actually receive if you claim benefits at age 62 (the earliest age at which you can claim retirement benefits), at age 66 (the “full retirement age” for those born from 1943 through 1954) and at age 70 (when benefits max out).

The box above shows the actual estimates for a 62-year-old who has earned at or above the Social Security wage base (the maximum subject to the Social Security tax each year) for most of his career. A glance at these numbers forcefully drives home the financial pain of the reduction in benefits for claiming at age 62 (compared with full retirement age) and the significant reward for waiting until age 70. The statement also serves as a quick reminder that Social Security is more than a retirement program. You’ll see an estimate of the monthly benefits you would receive starting right away if you were afflicted by a disability that prevents you from working for at least a year. There’s also an estimate of the survivor benefits your spouse and children could receive after your death.

In addition, the statement gives you a heads up about two rules that could potentially reduce your benefit below the estimates. One is the windfall elimination provision (WEP), which can crimp your benefit if you also receive a pension from a job where your wages were not taxed by Social Security (for example, some government and nonprofit jobs). The other potential squeeze comes from the government pension offset (GPO), which can affect your benefits as a spouse, widow or widower if you also receive a pension from federal, state or local government employment that was not covered by Social Security.

Understanding The Statement

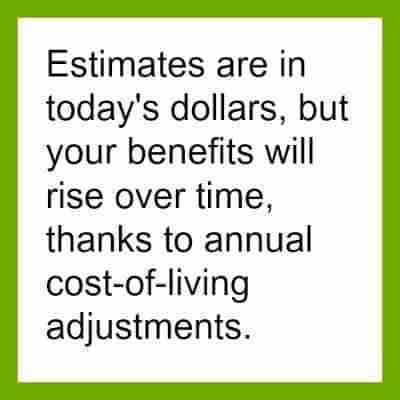

There are a couple of things to keep in mind as you contemplate the numbers on your statement. First, the calculations assume that between now and the time you claim benefits, you will continue to earn the same amount each year as you did in the most recent year for which earnings have been recorded. If you earn more, then your benefits could be higher; if you earn less, then your benefits could fall below the estimate. Also, the estimates on the statement are in current dollars. Your benefits will increase to keep up with inflation, thanks to annual cost-of-living adjustments (COLAs). Let’s say your statement estimates that you will receive $2,000 a month if you retire in ten years at age 66. If COLAs average 3% a year between now and then, your adjusted monthly benefit would be close to $2,700. (Of course, because the increases are designed to simply keep up with inflation, that $2,700 wouldn’t necessarily go any further than $2,000 goes today.)

Check Your Earning Record

Your statement will present some fascinating financial history: a complete lifetime record of your earnings. At least, you hope it’s complete. You’ll see a year-by-year listing of all your earnings that have been taxed by Social Security and Medicare. It can be entertaining: Remember how much (er, how little) you were earning back in 1980? The real point, of course, is to make sure you’ve received credit for all the taxes you’ve paid over the years. Your benefits are based on your highest 35 years of earnings, so you’ll be shorted if some of your earnings have not been posted to your account. If you spot an error—zero earnings recorded for a year you know you worked in a covered job, for example—call 800-772-1213 to get the ball rolling toward getting it fixed. You’ll want to check your record at least once a year to guard against errors and get the latest update on your estimated benefits. Also, note that the closer you get to claiming benefits, the more accurate the estimates become.

Douglas Finley, MS, CFP, AEP, CDFA founded Finley Wealth Advisors in February of 2006, as a Fiduciary Fee-Only Registered Investment Advisor, with the goal of creating a firm that eliminated the conflicts of interest inherent in the financial planner – advisor/client relationship. The firm specializes in wealth management for the middle-class millionaire.